How to Finance a Commercial Griddle for Your Restaurant

Let’s be honest, a new commercial griddle is more than just a piece of steel. It's the heart of your kitchen, the workhorse that pumps out perfect pancakes for the breakfast rush and sears burgers for the dinner crowd. Thinking about how to pay for it isn't just about the expense—it's a strategic move to get that money-making machine on your line without killing your cash flow. We'll walk you through exactly how to do it.

Why Smart Griddle Financing Is a Game Changer

That shiny new griddle you’ve got your eye on is a major upgrade. It means faster service, better consistency, and maybe even a few new items on the menu. But dropping $2,000 to over $10,000 in one go can put a serious squeeze on your bank account—money that’s better spent on payroll, inventory, or getting the word out.

This is exactly why figuring out how to finance a commercial griddle is such a crucial skill for any owner. Instead of dumping a huge chunk of cash at once, financing lets you break down the cost into smaller, predictable monthly payments.

Preserve Your Precious Cash Flow

Cash flow is everything in the restaurant business. We all know it. A big, upfront purchase can leave you scrambling if an unexpected repair pops up or a supplier raises prices. Financing keeps that essential cash buffer safe for the day-to-day grind.

Think about it this way: you’re launching a new brunch menu. You could pay $5,000 cash for a new griddle, or you could finance it for something like $150 a month. That frees up thousands of dollars right now to pour back into your launch. You could use it for:

- High-quality ingredients like local eggs and artisan bacon.

- Running some social media ads to promote the new menu.

- Bringing in an extra server to handle the weekend rush.

By financing, you're not just buying a griddle; you're investing in the entire success of your new menu rollout. It turns a major capital expenditure into a predictable operating expense, making budgeting far more straightforward.

Access Better Equipment Sooner

Putting off a much-needed griddle upgrade because you're short on cash can actually cost you more in the long run. An old, tired unit leads to unevenly cooked food, frustrated cooks, and higher energy bills. It’s a slow bleed.

Financing closes that gap, letting you get the high-performance griddle you need right now.

You can immediately start taking advantage of modern features like precise thermostatic controls or a thicker, heat-retaining griddle plate. Those aren't just bells and whistles; they translate directly into better food quality and a less chaotic kitchen. Ultimately, that makes its way to your bottom line. You get the benefits of a top-tier griddle while paying for it with the new revenue it helps you bring in. It's a simple, powerful way to grow.

Preparing Your Griddle Financing Application

Ever walked into a dinner rush without prepping a single ingredient? Of course not. It would be chaos. Walking into a lender's office unprepared is pretty much the same thing—it rarely ends well. Before you even think about applying for financing for that shiny new griddle, you need to get your story straight and your paperwork in order. This isn't just about getting a "yes"; it's about getting the best yes, with terms that won't cripple your cash flow.

It all starts with knowing exactly what you need. A high-volume diner flipping hundreds of burgers an hour has a totally different need than a small café looking to launch a weekend brunch menu. Don't just tell a lender, "I need a griddle." Get specific. Are we talking about a 36-inch gas model with thermostatic controls? Or will a 24-inch electric countertop unit get the job done? Your answer has a direct impact on the price tag and the loan you'll need.

Define Your Griddle and Budgetary Needs

First things first: take a hard, honest look at what your kitchen actually requires. The wrong griddle creates bottlenecks, wastes energy, and ultimately costs you money. Our own commercial kitchen equipment checklist is a great starting point to help you match your menu and volume with the right piece of equipment.

Once you’ve zeroed in on the perfect griddle, remember that the sticker price is just the beginning. Lenders love to see that you've thought through the total cost of ownership. It shows you're a serious operator.

- Installation Costs: Does your kitchen need a new gas line run? Maybe an upgraded electrical circuit? These can easily add hundreds, if not thousands, to your final bill.

- Ventilation Requirements: Commercial griddles need proper ventilation hoods. If you’re upgrading or installing one from scratch, that’s a significant expense to factor in.

- Ongoing Utility Bills: That beast of a gas griddle is going to hit your utility bill differently than an electric model. Project those recurring costs so a lender knows you've done your homework.

- Maintenance and Supplies: Don't forget the little things. You'll need cleaning supplies, new spatulas, and a rainy-day fund for potential repairs.

Mapping out a detailed budget like this signals that you're a responsible borrower who understands the long-term financial picture, not just the upfront purchase.

Gathering Your Essential Financial Documents

With your needs and budget locked down, it's time to gather your documents. Think of it as building a case for your restaurant's success. Your goal is to hand a lender a folder that tells a clear, compelling story about your financial health. Having everything ready to go makes the whole process smoother and marks you as a pro.

Lenders are paid to avoid risk. A complete, organized application package that clearly shows your restaurant is stable and can handle the new payments is the best tool you have for building their confidence.

Getting your financing sorted now is also just smart timing. The market for restaurant equipment is growing, with projections showing a steady increase in demand. Sorting out your financing today puts you in a prime position to ride that wave.

Your Document Checklist

This is your prep list for the loan application. While every lender is a little different, this core set of documents will get you 90% of the way there with most of them:

- Business Plan: If you're a new spot, this is non-negotiable. It needs to cover your concept, target market, and marketing plan. For established restaurants, it should explain exactly how this new griddle will boost revenue or cut costs.

- Profit & Loss (P&L) Statements: Have at least two years' worth of P&L statements ready. This is the clearest picture of your restaurant's profitability over time.

- Recent Bank Statements: Lenders will want to see three to six months of business bank statements. They're looking at your average daily balance and your overall cash flow patterns.

- Cash Flow Projections: Build out a realistic 12-month projection that shows how you'll manage your finances with the new loan payment. Make sure to include the extra revenue you expect the griddle to generate.

- Business and Personal Tax Returns: You'll almost certainly need the last two years of both personal and business tax returns to verify your income and financial history.

- Business Licenses and Registrations: Keep copies of your permits, licenses, and any legal formation documents (like articles of incorporation) handy.

Having this stack of documents ready to go shows you're serious and organized. It sets the foundation for a successful application and gives you a much stronger hand to play when it's time to negotiate.

Comparing Financing Options for Your Commercial Griddle

Deciding how to pay for your new griddle isn't just about the monthly payment. It's a strategic move that affects your restaurant's cash flow, tax situation, and even your ability to expand down the line. There are a few different ways to get that new flat-top onto your line, and understanding the real-world differences is crucial to avoid a costly wrong turn.

Let's walk through the most common ways to finance a griddle so you can pick the one that actually fits your restaurant's reality.

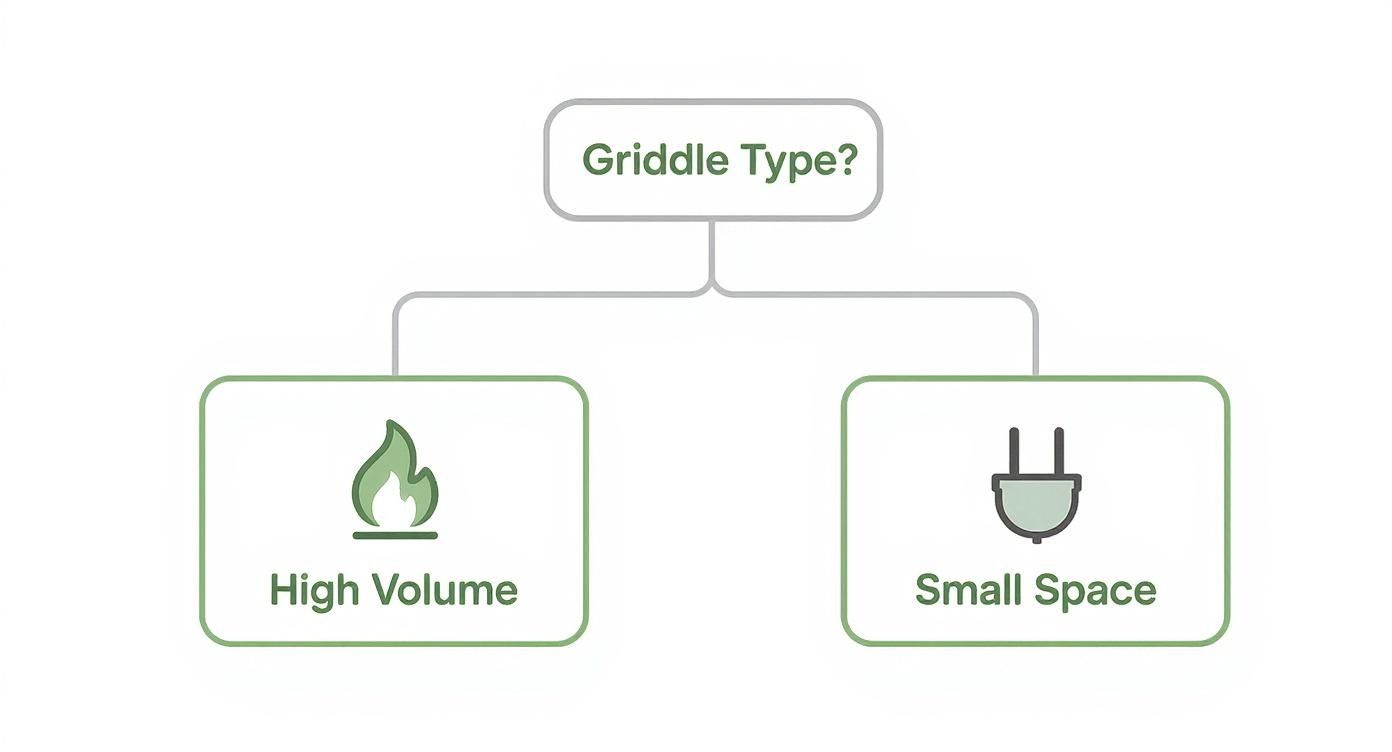

Before you even think about money, you need to know what you're buying. This simple decision tree can help you narrow down the type of griddle that makes sense for your kitchen's workflow.

As you can see, it often boils down to a fundamental choice: high-output gas griddles are workhorses for busy kitchens, while electric models give you flexibility in smaller spots or for specialized menu items.

Traditional Equipment Loans

An equipment loan is the most straightforward route. A lender gives you the cash to buy the griddle, and you pay it back in fixed monthly chunks over an agreed-upon term. Simple. The griddle itself acts as collateral, which often makes these loans a bit easier to get than other types of business funding.

The biggest win here is ownership. Once that final payment is made, the griddle is 100% yours. It becomes an asset on your books, and you can often claim depreciation on your taxes—a nice perk. This is usually the best path for established restaurants with solid credit and steady cash flow who know they'll be using that griddle for years to come.

Equipment Leasing: A Flexible Alternative

Think of leasing as a long-term rental. You make monthly payments to use the griddle for a set period, usually 12 to 60 months. When the lease is up, you typically have a few choices: buy the equipment (often for a pre-set price), send it back, or lease a brand-new model.

The main attraction of leasing is the lower upfront cost and smaller monthly payments. This keeps more of your cash free for day-to-day needs like payroll and inventory. It's a fantastic option for new restaurants working with limited startup capital or for kitchens that want the latest tech without being locked into ownership. Just remember, you’re not building equity, but the lease payments are usually fully tax-deductible as an operating expense.

It really comes down to this: Is building an asset more important than protecting your immediate cash flow? Answering that honestly is the key to making the right call for your business.

To make things even clearer, let's put the most common options side-by-side. This table gives you a quick snapshot of how these financing methods stack up against each other.

Financing Options for a Commercial Griddle at a Glance

| Financing Option | Typical Interest Rate / Cost | Ownership | Best For |

|---|---|---|---|

| Equipment Loan | 6% - 20% | Yes, after final payment | Established businesses with good credit wanting to build assets. |

| Equipment Lease | 8% - 30% (Factor Rate) | No, option to buy later | Startups or businesses wanting low upfront costs and flexibility. |

| SBA Loan | Prime + 2.75% - 4.75% | Yes | Well-qualified borrowers who can wait through a longer application process. |

| Vendor Financing | Varies widely | Varies (Loan or Lease) | Buyers looking for convenience and a streamlined process. |

| Merchant Cash Advance | 40% - 350% (APR) | Yes | Businesses needing immediate emergency cash with no other options. |

Looking at the numbers in black and white can really crystallize which path aligns with your financial strategy and risk tolerance. Each has its place, but they serve very different needs.

Exploring Other Financing Avenues

Beyond the big two, a few other paths can get you the griddle you need. Each one is designed for a specific situation.

- SBA Loans: These government-backed loans through the Small Business Administration often have great interest rates and long repayment terms. The trade-off? The application process is famously detailed and can take a lot more time and paperwork.

- Vendor Financing: This is when the griddle supplier—like us here at Griddles.com—offers financing directly. It’s incredibly convenient because you handle the purchase and the financing all in one place. It cuts out the middleman and simplifies everything.

- Merchant Cash Advance (MCA): An MCA gives you a lump sum of cash now in return for a cut of your future credit card sales. It's fast and easy to get, even with bad credit, but it's also by far the most expensive option. Think of an MCA as a last-resort, emergency-only button.

A griddle is a kitchen cornerstone, but it's just one piece of the puzzle. As you map out your financing, our commercial kitchen equipment list can help you budget for other essentials you'll need. Showing a lender you've thought through the whole setup, not just one item, makes your application that much stronger.

Ultimately, there's no single "best" option. The right choice is the one that fits your credit, your time in business, and your restaurant's financial game plan.

How to Secure the Best Terms on Your Loan or Lease

Getting an approval for financing feels great, but the real win is walking away with a deal that actually helps your bottom line. This is where you can save yourself thousands of dollars with just a little prep work. Let's talk about how to sit down at the negotiating table with confidence and get the best possible terms for your new commercial griddle.

Your power in any negotiation comes down to the strength of your application. When a lender sees a solid business plan, clean financials, and a good credit history, they see you as a low-risk partner. That's your leverage.

Don’t be shy about using it. Casually mention your steady sales growth or point to the detailed cash flow projections you've already mapped out. Frame the entire conversation around how reliable you are as a borrower.

Understanding What's on the Table

A lot of restaurant owners think financing terms are non-negotiable. The truth is, many parts of a loan or lease are flexible, especially when you've put together a strong application. Knowing what to ask for is half the battle.

Here are the areas where you often have some wiggle room:

- Interest Rate: This is the big one. Even a tiny reduction here can mean significant savings over the life of the loan.

- Down Payment: If your credit and business history are rock-solid, some lenders might lower the initial down payment, which keeps more cash in your pocket for operations.

- Loan or Lease Term: It's less common, but you might be able to adjust the length of the term by a few months to better align with your monthly budget.

- Prepayment Penalties: Always ask if you’ll be penalized for paying off the loan early. If there are penalties, push to have them reduced or, better yet, removed completely.

Your goal isn't to be a pain; it's to find a fair deal. Lenders want to work with serious operators. When you show up knowing your numbers and what you're talking about, you earn their respect—and often, their flexibility.

Don't forget that the market for restaurant equipment is hot. The global restaurant equipment market is expected to jump from USD 3.88 billion in 2024 to USD 4.2 billion in 2025. This growth is fueled by customers wanting faster service and more interesting menus—exactly what a new griddle delivers. All this means lenders are competing for your business, putting you in a much stronger position than you might realize. You can check out more on this market growth at OpenPR.com.

What This Looks Like in Real Dollars

Let’s run some numbers to see how this plays out. Say you’re financing a $10,000 commercial gas griddle on a five-year (60-month) term. The lender’s first offer comes in at 9% interest.

You do your homework, present your case well, and negotiate that rate down by just one point to 8%. Here's the difference that makes.

Scenario 1: The Initial 9% Offer

- Monthly Payment: About $207.58

- Total Interest Paid: $2,454.97

- Total Repayment: $12,454.97

Scenario 2: The Negotiated 8% Rate

- Monthly Payment: About $202.76

- Total Interest Paid: $2,165.84

- Total Repayment: $12,165.84

That single percentage point just saved you $289.13 over the life of the loan. It might not sound like life-changing money, but that’s cash that goes straight back into your business. That's enough for a new set of premium spatulas, a professional knife sharpening service for the whole kitchen, or a social media ad campaign to show off your new menu. Every single dollar counts.

Final Tips Before You Sign on the Dotted Line

Before you put pen to paper, read every last word of that contract. Really focus on the fine print—things like hidden fees, late payment penalties, and what happens if you default. If there’s any language you don’t understand, ask them to clarify it for you in an email.

And my most important piece of advice: get multiple offers. Never take the first deal you’re offered. Having competing offers is your single best negotiation tool. You can go back to Lender A and tell them what Lender B is offering. Ask if they can match it or beat it. This one simple step ensures you're getting a fair rate and not just leaving money on the table.

From Approved Funding to Firing Up Your New Griddle

Getting your financing approved is a huge win, but you're not done just yet. The real work begins now: getting that new griddle into your kitchen, seasoned, and making you money. This is where all your planning turns into reality, bridging the gap between a signed loan document and a kitchen that runs better than ever.

First up, you need to connect your lender with your griddle supplier. This isn't just about sending money; it’s a coordinated handoff to make sure the funds go to the right place and your purchase order gets finalized without a hitch. Keep the lines of communication wide open between all three parties.

Finalizing the Transaction

Your lender will have their own way of doing things, whether that’s wiring the funds directly to the vendor or cutting a check. Find out their exact process and give your vendor the lender’s contact info right away. A little proactivity here can prevent frustrating delays in shipping.

Before anything gets paid, give that final purchase order one last look. Seriously, don't skip this.

- Confirm the model number and specs. Make sure you’re getting the exact griddle you planned for.

- Check the delivery address and contact person. You don't want your new griddle ending up at the wrong loading dock.

- Triple-check the total cost. It needs to match your financing agreement to the penny.

Think of this as your final pre-shift huddle. A few minutes of confirmation now ensures a smooth service later, preventing costly errors and keeping your timeline on track.

Preparing Your Kitchen for Arrival

While the money is moving, you should be getting your kitchen ready. You can’t just plop a new commercial griddle down and expect it to work. Proper prep is crucial for a safe, efficient installation and to keep your downtime to a minimum.

This is a smart investment in your kitchen’s future, and you're not alone. The entire food service equipment market, valued at around USD 39.07 billion in 2024, is expected to climb to USD 58.22 billion by 2030. New kitchen gear, just like your griddle, is a massive part of that growth. You can see more details on this trend over at Market Research Future.

Before that delivery truck pulls up, run through this quick checklist:

- Utility Hookups: Is the gas line ready to go? Does the electrical outlet match the griddle’s voltage and amperage? Don’t guess—hire a pro to verify this stuff. It's a non-negotiable part of the process.

- Space and Ventilation: Measure the spot for the griddle one last time. You need enough clearance on all sides for safety and cleaning. Most importantly, is your ventilation hood powerful enough for this new unit?

- Delivery Path: Walk the route from the loading dock to the kitchen line. Clear out any junk, measure doorways, and make sure there’s a clear path. The delivery team will thank you.

Once your griddle is in place, the first thing you need to do is season it correctly. This step is absolutely vital for performance and making the equipment last. A little effort upfront guarantees that perfect non-stick surface and incredible results from day one.

Common Questions About Financing a Commercial Griddle

Jumping into the financing world can feel a little overwhelming, especially when you’re just trying to get a vital piece of equipment like a new griddle on the line. We get it. Here are some straightforward answers to the questions we hear most often from restaurant owners just like you.

What Credit Score Do I Need for Griddle Financing?

This is usually the first thing on everyone's mind. While there isn't one magic number, your credit score is the lender's first look at your financial track record. A better score shows you're a lower risk, which naturally opens the door to better interest rates and terms.

For most traditional equipment loans, lenders are looking for a personal credit score of at least 650. If you're sitting above 680, you're in a great spot to negotiate. But don't sweat it if you're not quite there. Plenty of alternative lenders and leasing companies are more flexible and might approve scores as low as 600, especially if your restaurant has solid revenue or you’ve been in business for a while.

Your credit score is just the starting point, not the whole story. Lenders also look at your time in business, your restaurant's cash flow, and its overall financial health. A strong, profitable business can often make up for a less-than-perfect credit score.

Can a Startup Restaurant Get Approved for a Griddle Lease?

Absolutely. In fact, leasing is a classic move for new restaurants trying to protect that precious startup cash. Lenders know a brand-new business won't have years of financials to show, so they just focus on other things.

For a startup, a lender will zero in on:

- Your Business Plan: They need to see a clear, well-thought-out plan. Show them your concept, who you're selling to, and your realistic financial projections.

- Personal Financial Strength: With no business history, your personal credit and finances will do a lot of the talking.

- Industry Experience: If you or your partners know your way around a kitchen and have run a successful restaurant before, that’s a huge vote of confidence.

Leasing is often easier for startups because the griddle itself is the collateral. Since the leasing company owns the equipment, their risk is lower if things don't go as planned. It’s a very common and practical way to get top-notch gear in your kitchen from day one.

How Do Taxes Differ Between a Loan and a Lease?

This is a big one. Understanding the tax differences between buying and leasing can seriously impact your bottom line, and one option might fit your financial strategy better than the other.

When you take out an equipment loan, you own the griddle immediately. You can't write off the monthly payments, but you get something else: depreciation. Thanks to Section 179 of the tax code, you might be able to deduct the entire purchase price of the griddle in the year you start using it. That can be a huge tax break right out of the gate.

On the flip side, with a true lease (also called an operating lease), you're basically renting the griddle. You don't own it, so you can typically deduct the full monthly lease payment as a standard business expense. This gives you a steady, predictable deduction month after month.

Here’s a simple way to look at it:

| Aspect | Equipment Loan (You Buy) | Operating Lease (You Rent) |

|---|---|---|

| Ownership | You own the griddle. | The leasing company owns it. |

| Tax Treatment | Claim depreciation (potentially a large upfront deduction). | Deduct the monthly payments as an operating expense. |

| Best For | Building assets and taking a big, one-time tax deduction. | Lowering taxable income with consistent monthly write-offs. |

Of course, it's always smart to run this by your accountant. They can help you figure out which strategy—a big depreciation deduction or steady monthly write-offs—will save you more money.

What Is a Typical Timeline from Application to Funding?

How quickly you can get the cash depends a lot on the financing route you take and how organized you are. When you need a griddle yesterday, speed matters.

- Online Lenders and Leases: This is almost always your fastest option. If you have all your paperwork ready, you can get approved in as little as 24 to 48 hours. The money can show up just as fast, sometimes even the same day you're approved.

- Traditional Bank Loans: Banks are thorough, and that takes time. Plan on the process taking anywhere from two weeks to a month, and sometimes longer if there are any hiccups.

- SBA Loans: These loans have fantastic terms, but they are famous for their lengthy process. It's not unusual for an SBA loan to take 30 to 90 days from application to funding.

The best way to speed things up, no matter who you're working with, is to be prepared. Get your bank statements, profit and loss reports, and tax returns organized before you even apply. A clean, complete application is the number one thing you can do to get your funding faster.

Ready to find the perfect griddle for your kitchen? At Griddles.com, we not only offer a wide selection of top-quality commercial griddles but also provide flexible payment options to help you get the equipment you need. Explore our catalog and equip your restaurant for success today.