Financing Your Commercial Griddle: A Complete Guide

A quality commercial griddle is the heart of any kitchen, but that kind of high-performance gear doesn't come cheap. That’s where financing a commercial griddle comes in. It’s a smart way to get the equipment you need without wiping out your bank account, bridging the gap between your culinary dreams and your day-to-day reality.

By financing, you can hang onto your cash for critical things like payroll and inventory while immediately upgrading your kitchen's power.

Why Financing Your Commercial Griddle Is a Smart Move

Picture your kitchen running at peak efficiency. The high-capacity commercial griddle you've been dreaming of isn't just another piece of metal; it’s the ticket to shaving minutes off ticket times, delivering a perfectly consistent product, and maybe even adding new items to your menu.

But let's be real—the price tag on a top-tier commercial griddle forces a tough decision between holding onto cash and investing in quality. This is exactly why financing a commercial griddle is such a powerful tool for savvy operators.

Financing acts like a bridge, connecting your immediate needs with your long-term vision. Instead of one huge upfront payment that drains your cash reserves, you spread the cost out into predictable monthly payments. A major purchase becomes a manageable operating expense.

Preserve Your Precious Capital

The biggest win here is simple: you keep your cash. In the food business, whether you're running a restaurant, food truck, or ghost kitchen, cash is everything. It’s the fuel that keeps the engine running every single day.

- Inventory and Supplies: Making sure you’re never caught without key ingredients during the Friday night rush.

- Payroll: Keeping your all-star team happy, paid, and focused.

- Marketing: Getting the word out and bringing new faces through the door.

- Unexpected Repairs: Handling a busted walk-in or a leaky pipe without breaking a sweat.

When you finance your commercial griddle, your capital stays liquid, ready to be used wherever it’s most needed. It keeps your business nimble and ready for anything.

Think of it this way: Financing lets your money do two jobs at once. The new commercial griddle is busy making you money, while your cash on hand is taking care of daily operations and jumping on new opportunities.

A Growing Market Driven by Need

This isn't just a niche strategy; it's how the industry grows. The global restaurant equipment market is booming, expected to jump from USD 4.8 billion in 2025 to a staggering USD 10.2 billion by 2035.

That explosive growth shows that restaurants everywhere are using financing to get the gear they need without putting the brakes on their business. You can learn more about the trends in the restaurant equipment market and see just how vital financing has become.

At the end of the day, financing a commercial griddle isn't just about going into debt. It’s a calculated investment in your kitchen’s future, boosting both your efficiency and your bottom line. It lets you get the workhorse you need right now so you can start cooking more and earning more, immediately.

Choosing the Right Financing Path for Your Griddle

You’ve found the perfect commercial griddle for your kitchen—the one that’s going to churn out perfect pancakes and sizzling burgers day after day. Great! Now, how are you going to pay for it? It can feel a bit like staring down a complex recipe, but trust me, it’s simpler than it looks.

When it comes to getting that new griddle onto your line, you’ve got a few clear paths. Let's walk through them to find the one that makes the most sense for your restaurant's cash flow and long-term goals.

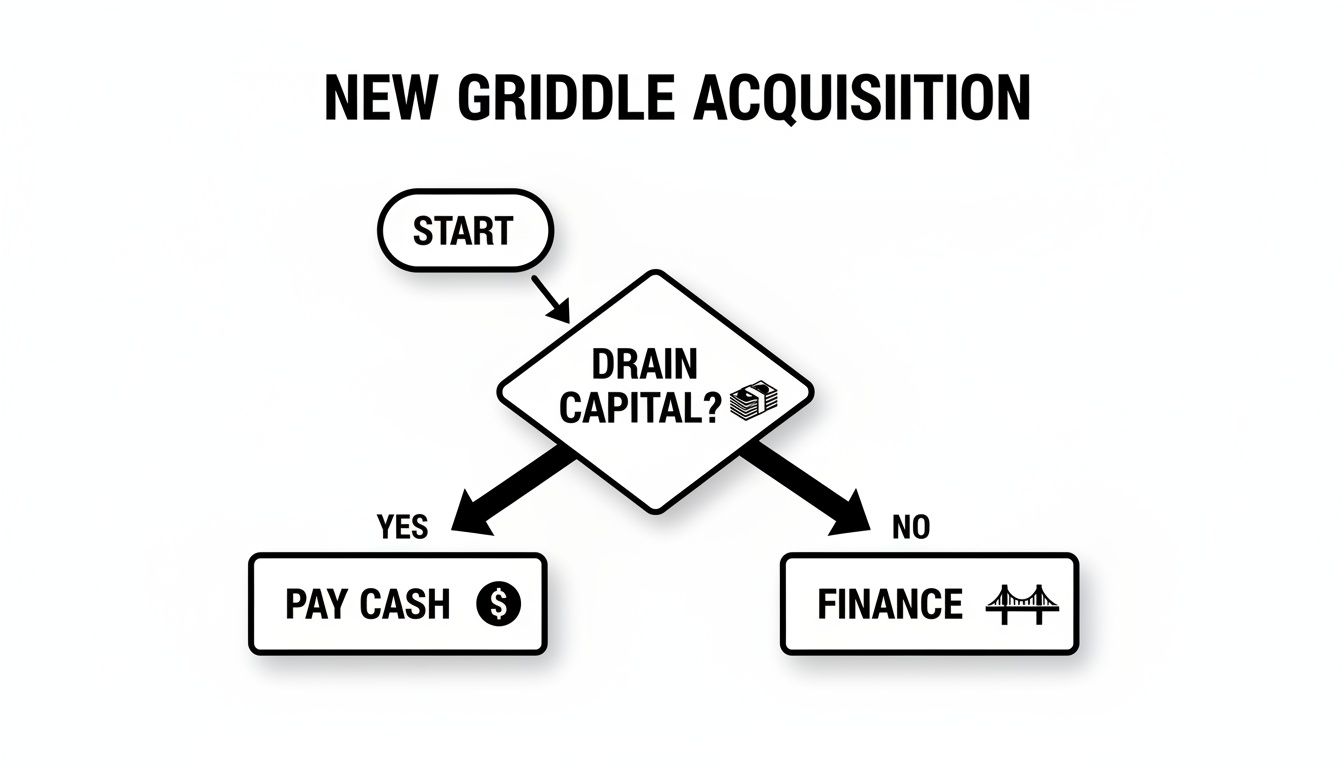

The very first decision is a big one: pay for it all upfront with cash, or finance it over time? This flowchart breaks down that fundamental choice every kitchen operator has to make.

As you can see, if draining your working capital isn't an option (and for most of us, it isn't), financing is the bridge that gets you the gear you need without putting your financial health at risk.

Equipment Financing Agreements (EFAs)

Think of an Equipment Financing Agreement (EFA) as a car loan, but for your griddle. It's straightforward: you borrow a specific amount of money to buy a specific commercial griddle, and that shiny new griddle serves as collateral for the loan.

Because the griddle itself secures the loan, lenders see these as a lower-risk deal. That often means you can snag better interest rates and terms, even if your business is still pretty new. Plus, the payments are fixed, so you know exactly what you owe each month—no surprises.

- Best For: Any operation—restaurants, food trucks, ghost kitchens—that wants to own their commercial griddle and build equity in their assets.

- Typical Terms: Most EFAs run for 2 to 5 years, with interest rates depending on your business's credit and track record.

- Key Advantage: It's simple, and it leads to ownership. Once that last payment is made, the griddle is 100% yours.

Traditional Business Loans

A traditional business loan gives you a bit more breathing room than an EFA. Instead of being tied to one specific griddle, you get a lump sum of cash to use for whatever your business needs, including that new flat-top.

This is a fantastic option if you're doing a bigger overhaul—maybe you need a new griddle and a new ventilation hood or some prep tables. The catch? These loans are often unsecured, which means lenders will want to see a stronger credit history and more of your financial paperwork before they sign off.

SBA Loans for Commercial Griddles

Let's talk about the heavy hitters. Backed by the U.S. Small Business Administration (SBA), these loans are specifically designed to help small businesses like yours get a leg up. The government guarantees a portion of the loan, which makes lenders feel a lot more comfortable.

The result? SBA loans often come with the best interest rates and longest repayment terms you can find. The application process is a lot like applying for a mortgage—it’s thorough and you'll need your ducks in a row with a solid business plan and financials. But if you qualify, the amazing terms make a big purchase much easier to handle.

There’s a reason the equipment finance industry hit a record $1.34 trillion in 2023. About 82% of businesses, including countless restaurant owners, use financing to get the equipment they need. With more than half of restaurants planning to spend more on equipment, financing is what fuels that growth.

Leasing Your Commercial Griddle

So, what if you're not ready for the long-term commitment of ownership? That's where leasing comes in. It’s like renting an apartment instead of buying a house. You pay a fixed monthly fee to use a brand-new, top-of-the-line griddle for a set period, usually a few years.

This route is perfect for restaurants that want to always have the latest tech or those who need to keep upfront costs as low as possible. When the lease is up, you’ve got options:

- Return the griddle and get a brand-new model.

- Buy the griddle for its current market value.

- Extend your lease.

Exploring commercial leasing options is a smart move for many businesses because it keeps cash in your pocket while giving you the flexibility to adapt as your menu and kitchen evolve. Each of these financing paths offers its own set of advantages, so you can pick the strategy that truly fits your restaurant's budget, ambitions, and style.

Your Step-By-Step Griddle Financing Application Checklist

Want to know the secret to a successful financing application? It’s all about preparation. While applying for a loan for that shiny new commercial griddle can feel like a mountain of work, breaking it down into a simple checklist makes it manageable. This isn’t about jumping through hoops; it’s about telling a clear, compelling story about your business's financial health and future.

Lenders aren't just staring at numbers on a page. They're looking for a professional, organized operator who has a firm handle on their business. When you hand them a complete, tidy application package, it immediately sends a strong signal: you're a serious partner worth investing in. This checklist will walk you through gathering every document you need to present a polished and confident case.

Gathering Your Core Business Documents

First things first, let's round up the foundational paperwork. These are the documents that prove your business is a legitimate, properly structured operation. Think of them as your business's birth certificate and ID.

-

Business Plan: This is your restaurant's story and its roadmap. It needs to lay out your concept, who you're serving, and your financial projections. Most importantly, you need to connect the dots and show exactly how this new griddle will boost revenue or efficiency—maybe it unlocks a killer breakfast menu or lets you shave minutes off your lunch rush ticket times.

-

Business Licenses and Permits: Get copies of your business registration, food service permits, and any other licenses your city or state requires. This is non-negotiable proof that you're operating by the book.

-

Lease Agreement: If you rent your kitchen space, the lender will definitely want to see your lease. It confirms your physical location and shows that you have a stable home for your operations for the duration of the loan.

These documents set the stage. They establish that your business is real, legal, and has a vision for success. They are the bedrock of your entire application.

Showcasing Your Financial Health

Alright, now for the numbers. You need to paint a clear picture of your restaurant’s financial performance. This is where lenders look to see if you can comfortably handle the monthly payments on your new griddle. Honesty and accuracy are everything here.

Think of your financial documents as a health checkup for your business. A strong Profit & Loss statement shows your business is profitable, while healthy bank statements prove you have the cash flow to manage day-to-day operations and new debt.

Here’s the financial paperwork you’ll need to get in order:

- Recent Bank Statements: Pull together your last three to six months of business bank statements. Lenders pour over these to understand your cash flow, average daily balance, and revenue patterns. It’s the most direct evidence that you can manage another monthly payment.

- Profit & Loss (P&L) Statement: Often called an income statement, your P&L breaks down your revenues, costs, and profit over a set period. Be prepared to provide P&Ls for the last one or two years.

- Balance Sheet: This is a snapshot of your business's assets, liabilities, and owner's equity at a specific moment in time. It gives the lender a sense of your operation's overall financial stability.

- Business and Personal Tax Returns: Nearly all lenders will ask for the last two years of both your business and personal tax returns. This verifies your reported income and gives them a longer-term view of your financial history.

Having these documents organized and ready to go will make the approval process so much smoother. For a deeper dive into organizing your kitchen needs before you even think about financing, check out our complete commercial kitchen equipment checklist.

The Final Piece: The Griddle Quote

Last but not least, you need the specifics of the griddle you want to buy. You can't get a loan for a vague idea; lenders need to see a professional, itemized quote for the exact commercial griddle you've picked out.

Make sure the quote is from a reputable supplier and clearly includes:

- The exact make and model of the griddle.

- The total cost, including any taxes, shipping fees, or installation charges.

- The supplier's full contact information and business details.

This quote is the anchor for the entire financing agreement. It defines the asset the lender is putting money against, connecting your business plan directly to a tangible piece of equipment. It shows the lender precisely where their investment is going and completes your application package.

How to Boost Your Financing Approval Odds

Getting the green light for your new commercial griddle isn't just about filling out paperwork. It's about painting a clear picture for lenders—one that shows you're a smart, reliable operator they can trust. With a few strategic moves, you can seriously improve your chances of not only getting approved but landing great terms.

This means going beyond the basic application. By putting a little extra effort into a few key areas, you can show lenders that investing in your kitchen is a win for everyone.

Strengthen Your Credit Score

Your credit score is the first number a lender will look at. Think of it as your financial handshake—it's a quick summary of how you've handled debt in the past. A higher score tells them you're a responsible borrower, which makes you a much lower risk.

Most lenders in the commercial griddle financing world want to see a score of at least 620, but the really good rates usually go to operators with a 680 or higher. Before you even start applying, take these steps:

- Check Your Score: Grab your score for free from services like Credit Karma or through your credit card provider.

- Review Your Report: Pull your full report and look for mistakes. An error could be dragging your score down, so dispute anything that looks off.

- Pay Down Balances: If your credit cards are carrying high balances, work on paying them down. This lowers your credit utilization and can give your score a nice bump.

A solid credit history is your best friend in the financing game. It opens up more options and better deals, making that new griddle much more affordable.

Make a Meaningful Down Payment

Putting some of your own money down on a new griddle speaks volumes to a lender. It shows you have "skin in the game" and are financially committed to making this purchase work. It also shrinks the loan amount, which naturally lowers the lender's risk.

A down payment demonstrates your financial stability and belief in the investment. Lenders see it as a sign of a serious, well-managed business that has the cash flow to support its growth plans.

Even a down payment of 10% to 20% can make a huge difference in getting approved. It also often unlocks better interest rates and repayment terms, which saves you real money over the life of the loan. It's one of the most important steps when financing a commercial griddle.

Craft a Compelling Business Narrative

Your business plan has to do more than just present numbers—it needs to tell a story. More specifically, it needs to draw a straight line from "buying a new griddle" to "making more money."

Don't just say you need a new griddle. Show them why.

- Increased Capacity: "Our new 48-inch griddle will let us double our breakfast output. We'll cut ticket times by three minutes during the morning rush and boost revenue by an estimated 15%."

- Menu Expansion: "This thermostatic griddle is key to launching our new gourmet burger and sandwich line, letting us tap into the busy lunch delivery market in our area."

- Improved Efficiency: "By replacing our old, tired unit, we project a 20% drop in gas usage and a huge reduction in food waste from hot spots."

When you connect the commercial griddle directly to profit, the loan stops looking like an expense and starts looking like a smart investment. For more ideas on structuring these deals, check out our in-depth guide on restaurant equipment financing.

Compare Multiple Financing Offers

Finally, never, ever take the first offer you get. The world of commercial griddle financing is competitive. You've got traditional banks, online lenders, and equipment specialists all wanting your business, and they all have different rates, terms, and hidden fees.

Make sure you get at least three different quotes to compare side-by-side. Look past the monthly payment and calculate the total cost of the loan. To help manage all the paperwork that comes with applications, you might look into automated document signing solutions. Shopping around is the only way to be sure you're getting the best possible deal for your restaurant.

Finding the Perfect Griddle for Your Financing Plan

You’ve already done the heavy lifting: you shored up your credit, saved up a down payment, and got all your financial paperwork in order. Now for the fun part—connecting all that hard work to the heart of your kitchen. The absolute cornerstone of a successful financing application is a professional, detailed quote for the specific commercial griddle you need.

This piece of paper does so much more than just list a price. It transforms your request from a vague idea into a concrete, tangible investment in the eyes of a lender. It shows them exactly where their money is going and what piece of equipment will secure the deal. A vague request gets a vague (and often negative) response, but a precise quote proves you're a serious, organized operator with a clear vision for growth.

Partnering with the Right Griddle Supplier

Let's be honest, navigating the world of commercial griddles can get complicated. You’re weighing size, gas versus electric, plate thickness, and thermostatic controls against manual ones. This is exactly why partnering with a knowledgeable vendor is a critical step in successfully financing a commercial griddle.

A good supplier is more than just a salesperson; they become a key player in your financing journey. They can help you dial in the perfect griddle for your kitchen's workflow and menu, making sure you don’t overspend on bells and whistles you don't need or, worse, underspend on a unit that can't keep up with your Saturday night rush.

A professional quote from a trusted vendor is your application’s anchor. It provides the clarity and legitimacy lenders require, showing them you’ve done your research and are ready to make a smart, informed investment in your restaurant's future.

Most importantly, they provide the official documentation that lenders absolutely require. This quote will spell out all the necessary details to satisfy any underwriter, including:

- Precise Model Specifications: The exact make, model number, and dimensions.

- Itemized Cost Breakdown: A clear list of the griddle’s price, plus any applicable taxes, shipping, and installation fees.

- Official Vendor Information: The supplier’s name, address, and contact details.

We Are Your Financing Partner

Think of us as part of your team. We’re here to help you get both the funding and the commercial griddle you need to win. Our experts are on standby to help you identify the perfect griddle for your operation and then provide a detailed, lender-ready quote to make your application package shine. To see how your new griddle fits into the bigger picture, check out a comprehensive commercial kitchen equipment list and make sure your entire line is ready for action.

We know the financing game inside and out, and we’re committed to giving you the professional paperwork needed to make your application as strong as it can be. We’re not just here to sell you a griddle; we’re here to help you build the kitchen of your dreams.

Answering Your Griddle Financing Questions

Even with a solid plan, a few questions always pop up when you get down to the nitty-gritty of financing. It's totally normal. Let's walk through some of the most common ones we hear from chefs and restaurant owners to clear things up.

Can I Finance a Used Commercial Griddle?

You bet. Financing a used commercial griddle is incredibly common, and honestly, it's a smart way to get a top-tier griddle without the brand-new price tag. Most lenders are completely on board with it.

They see a well-maintained, used griddle from a reputable brand as a solid investment. The key is making sure you're buying from a trusted source that can provide clear documentation on the griddle's condition and value. This gives the lender the confidence they need, knowing the griddle securing the loan is worth it.

What Credit Score Do I Need for Commercial Griddle Financing?

This is the big one, right? While every lender is a little different, a good benchmark to aim for is a personal credit score of 620 or higher. If you want the best rates and most flexible terms, lenders really love to see scores in the 680+ range.

But don't panic if your score isn't quite there. A lower score isn't an automatic "no." You can often strengthen your application in other ways:

- A solid down payment: Putting more money down shows you’re serious and lowers the lender's risk.

- Strong business financials: If you can show consistent revenue and good cash flow, it proves you can handle the payments, regardless of your personal score.

- Extra collateral: Sometimes, offering another business asset can help get a loan over the finish line.

How Quickly Can I Get Approved for a Griddle Loan or Lease?

In a busy kitchen, time is money, so this is a crucial question. The speed of approval really depends on who you're working with.

Online lenders and companies that specialize in commercial griddle financing are usually the fastest, sometimes giving you an answer in just 24 to 48 hours. On the flip side, traditional banks and SBA loans are much more thorough. Their underwriting process can take several weeks, or even a month, to complete. Your best bet for speeding things up is to have all your paperwork organized and ready to go from the start.

When a lease ends, you're at a crossroads with powerful options: you can upgrade to the newest model, buy the griddle you've grown to love, or just hand it back. That flexibility is a huge win for any business that needs to stay nimble.

What Are My Options at the End of a Griddle Lease Term?

When your lease is up, you've got choices. This flexibility is one of the biggest perks of leasing. Typically, you can:

- Buy the Griddle: You can purchase the griddle for its current market value or for a price you agreed on from day one (this is common in a "$1 buyout lease").

- Renew the Lease: Happy with your griddle? You can usually extend the lease, often with a lower monthly payment.

- Return the Griddle: Simply send the griddle back to the leasing company, no strings attached. This frees you up to lease a brand-new model with all the latest features.

Ready to find the perfect commercial griddle and get the professional quote you need for your financing application? At Griddles.com, our experts are here to help you select the right equipment for your kitchen and provide all the documentation you need for a successful application. Explore our full catalog and get started at https://griddles.com today.